Reviewed by Nick Craven, AVP Business & Consumer Banking

When crafting a strong, dependable plan for your finances, one of the foundational elements is a savings account. Creating a savings account allows one to build an emergency fund in case of a rainy day, and serves as a secure depository account to save for planned expenses, such as a family vacation, a new car, or a mortgage down payment. Setting aside enough money to address basic expenses gives you a valuable safety net to provide critical financial support in a scenario where you’re laid off or can’t work due to medical or other reasons. An emergency fund also provides peace of mind in everyday life, allowing you to relax and reassure yourself if your thoughts ever drift to considerations like “How would I pay my rent or mortgage if I was out of work for two months?”

Between building your emergency fund and saving up for big life events, a savings account is a secure way to store and grow your money accessibly. Let’s look at how much money is recommended to set aside, and why utilizing a savings account is a particularly effective approach.

Understanding the emergency fund

Your emergency fund should help you address expenses that are unpredictable, unavoidable, and have a major financial impact on your day-to-day and long-term existence. While the need for new tires or a regular tune-up for your car doesn’t quite qualify as an emergency fund expense, because they are predictable, there are plenty of auto maintenance issues that can’t reasonably be discovered ahead of time. Such issues would qualify as a legitimate emergency fund expense. Other legitimate – and more substantial – uses for an emergency fund include repairs to a home following a major weather event, paying basic bills like rent and utilities while out of work, and covering sudden medical expenses.

An emergency fund doesn’t just allow you to have money on hand to deal with unexpected circumstances, it also allows you to avoid the negatives that come along with alternative methods of accessing necessary funding. In situations where there are no other options, a high-interest credit card or personal loan can help keep you afloat. However, these options have obvious drawbacks. There’s the potential to not be approved for the card or loan, the delay that’s attached to the approval process, and, of course, the interest that must be paid in addition to the principal. By saving and setting aside money in advance, you reduce overall financial liability should a major, unforeseeable expense arise.

The general advice for emergency funds is to set aside an amount sufficient to cover your basic expenses for three to six months. That includes fixed costs, such as rent and utility bills, as well as variable costs such as groceries, gas, and other everyday needs. Because everyone’s financial situation is different, the best approach is to review your recent bills and spending in relevant categories and settle on a number that makes sense for your spending profile.

How much should I have in savings?

One of the most common questions people have about their emergency fund and non-emergency saving accounts is how much money they should keep in each. The answer to this question can vary depending on your age and life circumstances. In this article, we’ll explore some general guidelines for how much you should have in your savings account at each age.

In your 20s

Your 20s are a time when you’re likely just starting your career, and you may not have many financial obligations yet. If you’re in this age range, financial experts recommend that you aim to save up at least three months’ worth of living expenses in your emergency fund.

Your initial emergency fund should include enough money to cover your rent or mortgage, utilities, food, and other essentials. As you get older and your financial responsibilities grow, you may need to increase the amount to accommodate real and lifestyle inflation.

Once you have an established emergency fund, apply your surplus income toward paying off debts such as student loans, and invest in your future by making regular contributions to your retirement account(s).

In your 30s

By the time you’re in your 30s, you may have started a family or bought a home, which can lead to more financial responsibilities. At this age, experts recommend that you aim to have six months’ worth of living expenses saved in your emergency fund.

Your emergency fund may need to go beyond basic expenses and cover additional costs such as childcare or student loan payments. As with the recommended strategy of your 20s, you should first prioritize building an emergency fund that covers 1-3 months of your living expenses plus any loan or credit card payments. Having a nest egg will give you and your family a safety net in the case of an unfortunate event.

After you have an initial emergency fund established, use your surplus income to pay off any outstanding debts. Once your debts have been handled, continue building your emergency fund to cover at least six months of living expenses, increase your retirement contributions, and begin saving for larger planned expenditures.

In your 40s

In your 40s, you’re likely in the middle of your career and may have children who are getting ready to go to college. Experts recommend that you aim to save up at least nine months’ worth of living expenses in your emergency fund by the time you reach your 40s.

Having a healthy emergency fund can help prepare you for unexpected expenses such as a major home repair or a job loss. At this age, you can assess your ideal standard of living and calculate the amount of retirement savings needed to ensure you have a comfortable retirement. Between your projected retirement needs and other long-term financial goals, evaluate what changes need to be made in order to reach your savings objectives.

In your 50s and beyond

As you get closer to retirement age, it becomes even more important to have a solid emergency fund in place. Experts recommend that you aim to have a full year’s worth of living expenses saved up by the time you reach your 50s.

This can help you weather unexpected expenses or changes in your income as you near retirement age. It’s also a good time to revisit your retirement savings strategy and make sure you will have enough put away to support yourself in your golden years.

Of course, these are just general guidelines, and the right emergency fund strategy for you may vary depending on your circumstances. Factors like your job stability, debt load, and overall financial goals can all impact how you answer the question: how much should I have in savings?

How to build your savings account

Building up your savings can be a daunting task, but it is an essential part of achieving financial stability and security. Whether you’re saving for a specific goal or simply building a safety net for unexpected expenses, there are several effective ways to increase your savings over time.

Set a savings goal

The first step in building your savings is to set a clear and realistic savings goal. This could be a short-term goal, such as saving for a vacation, or a long-term goal, such as saving for retirement. Having a specific goal in mind will help you stay motivated and focused on your savings efforts.

Create a budget

Once you have set your savings goal, it is important to create a budget that will help you reach that goal. A budget will help you track your income and expenses and identify areas where you can cut back on spending to save more money.

Automate your savings

One of the easiest and most effective ways to build your savings is to automate the saving activity. This means setting up direct deposit to save a percentage of each paycheck, or scheduling automatic transfers from your checking account to your savings account on a regular basis. By automating your saving, you can ensure that you are consistently putting money aside without having to think about it.

Reduce expenses

Another aid to growing your savings is reducing your expenses. This could involve cutting back on unnecessary expenses, such as eating out or buying expensive clothing, or finding ways to save on necessary expenses, such as switching to a more affordable cell phone plan.

Increase income

Building your savings can also involve increasing your income. This could mean taking on a side job or freelance work, asking for a raise at your current job, or looking for a new position with opportunity for professional advancement.

Look for cashback opportunities

Cashback apps or rewards debit cards can be a great way to build your savings without having to make significant changes to your spending habits. These tools allow you to earn cash back on certain purchases and/or bill payments, which can then be deposited into your savings account.

Take advantage of employer benefits

If your employer offers retirement savings plans, such as a 401(k) or IRA, make sure to take advantage of the benefits. Many employers also offer matching contributions, which can significantly boost your savings, so always ask or read the benefit details to ensure you receive the maximum amount possible.

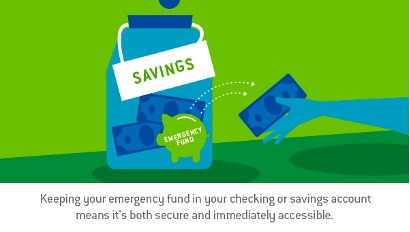

Why a savings account is a great place to keep your emergency fund

Saving the money that sits in your emergency fund is the most important task when it comes to this financial need, but finding a secure place to store it is a close second. When you keep your emergency fund in a savings account, you accomplish three key objectives: You make sure your money is liquid and ready to be accessed at any time, you leverage the Federal Deposit Insurance Corporation to keep it safe even in a worst-case economic scenario, and you are often able to earn interest on your money over time.

High Yield Savings Accounts are a type of savings account that can be especially beneficial for storing emergency funds. These typically offer a much higher interest rate than the national average for savings accounts, meaning that your deposited funds continue to earn and grow while remaining available to be used in case of emergency.

Because you can’t plan for the unexpected, savings accounts are especially powerful choices for keeping your emergency fund safe, stable, and accessible. Savings accounts also ensure you don’t accidentally dip into your emergency fund when making everyday purchases—keeping it in a separate account from your daily spending keeps it protected.

TAB Bank is proud to offer a range of accounts that can serve your regular checking and savings needs while also serving as effective vehicles for storing an emergency fund. Check out our personal banking options or get in touch for more information.